/MBL_JoshMennen_2022-01-12_300x300px.jpg)

Class actions

Global search

Life insurance might make you think of payouts after someone dies, but it's really any insurance product that you don’t renew each year – think of policies like disability insurance, income protection and death benefit insurance.

Making claims on these policies can often feel like an uphill battle, especially if the insurer disputes it. There are legal complexities and obstacles that leave people uncertain about what will happen, at a time when they need support most.

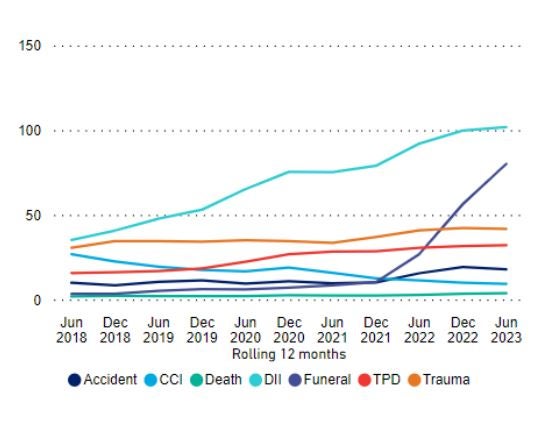

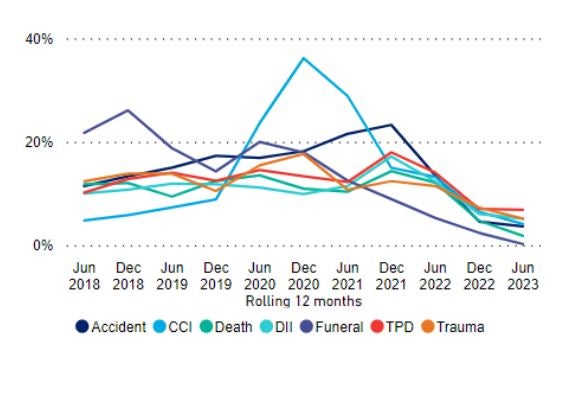

The recently released statistics from the Australian Prudential Regulation Authority (APRA) reveal the increase in insurance disputes and prolonged resolution times overall, which particularly impacts those claiming under policies purchased through financial advisers.

APRA's statistics reveal critical trends that highlight the difficulties for people making claims in the life insurance sector:

While many people have life insurance products automatically through their superannuation, some policies are purchased through financial advisers. Since June 2021 there has been a surge in disputed claims linked to these policies. This is an added stress for people claiming against these policies, and it often leads to prolonged conflicts and contentious resolution processes.

There's an alarming increase in disputes for income protection claims. Insurers are more inclined to terminate benefits for people who are already claiming, making their struggle for financial support during periods of disability even more difficult.

Source: Life insurance claims and disputes statistics, APRA

Source: Life insurance claims and disputes statistics, APRA

Since December 2021, there has been a significant decline in insurers reversing their decision after rejecting a claim. This trend highlights the growing difficulty to get insurers to reconsider their denials without resorting to legal action.

Data from the ASIC Moneysmart’s Life Insurance Claims Comparison Tool reveals significant differences in how insurers perform in responding to and approving claims, particularly in income protection and total and permanent disability (TPD) claims. Notably, some insurers display lower rates of claims accepted and higher rates of disputes compared to other insurers.

Some insurers show higher dispute rates compared to the industry average, which makes claims against policies from this insurer more challenging.

| Insurer | Claims accepted | Average claim time (months) | Disputes per 100,000 lives insured | Policy cancellation rate |

|---|---|---|---|---|

| Industry Average | 95.0% | 1.6 | 318.2 | 14.1% |

| Resolution Life | 96.9% | 2.1 | 1021.3 | 18.4% |

| Zurich | 93.3% | 1.7 | 416.9 | 13.3% |

| AIA | 94.7% | 1.6 | 287.5 | 18.7% |

| TAL | 95.1% | 1.2 | 209.4 | 11.8% |

| MLC | 95.7% | 1.4 | 189.8 | 14.0% |

| ClearView | 94.6% | 2.2 | 186.9 | 13.4% |

| TLIS | 95.8% | 1.6 | 176.3 | 13.2% |

| NobleOak | 98.3% | 1.8 | 17.4 | 5.8% |

| QBE/Integrity | ‡ | ‡ | ‡ | 8.4% |

| MetLife | ‡ | ‡ | ‡ | 5.4% |

Insurers with lower claims acceptance rates and longer claim times emphasizes the struggle people making claims face in securing their entitled benefits.

Following the Royal Commission, life insurers appear to be less worried about their image, as foreign-owned companies now largely control the industry. This shift makes them less sensitive to reputational damage, compared to previously influential Australian banks.

Companies like some listed, based in Bermuda and operating a 'closed book,' - meaning they don’t take on new business and policies - are reducing their concern for unreasonable claims assessment conduct and related reputational impacts.

Despite the industry's reported increase in profit and healthy return on net assets, people making claims continue to struggle with disputes and challenges to securing their benefits.

In the face of these complexities, our experienced Superannuation and Insurance Team is a supportive, guiding force and trusted partner.

Our expertise in insurance law, and successfully working on thousands of claims allows us to provide tailored strategies, and importantly, empathy and unwavering advocacy to ensure our clients receive the support they deserve.

Given the complexities in the APRA statistics, it can be crucial for people dealing with life insurance claims and disputes to have solid, experienced support from people who understand the law, inside and out.

Disclaimer: This blog post is for informational purposes only and is not legal advice. Readers are encouraged to seek professional legal counsel for their specific circumstances.

Contact us today

If you're unable to work due to illness or injury, you may be eligible to make a claim on your superannuation insurance. Your injury can be physical or psychological and doesn't need to be work-related. We can help you understand what options are available to you.

Read more about superannuation

/what-if-workcover-doesnt-cover-my-mental-health-claim-thumbnail.jpg)

/the-hidden-consequences-of-unpaid-super-thumbnail.jpg)

/financial-advisor-red-flags-thumbnail.jpg)

We are here to help. Give us a call, request a call back or use our free claim check tool to get in touch with our friendly legal team. With local knowledge and a national network of experts, we have the experience you can count on.

We have lawyers who specialise in a range of legal claims who travel to Australian Capital Territory. If you need a lawyer in Canberra or elsewhere in Australian Capital Territory, please call us on 1800 675 346.

We have lawyers who specialise in a range of legal claims who travel to Tasmania. If you need a lawyer in Hobart, Launceston or elsewhere in Tasmania, please call us on 1800 675 346.

/MBL_HayrireUluca_2022-01-14_300x300px.jpg)